Advertiser Disclosure: Eye of the Flyer, a division of Chatterbox Entertainment, Inc., is part of an affiliate sales network and and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed, or approved by any of these entities. Some links on this page are affiliate or referral links. We may receive a commission or referral bonus for purchases or successful applications made during shopping sessions or signups initiated from clicking those links. The content on this page is accurate as of the posting date; however, some of the offers mentioned may have expired.

It’s that time again and time for, more or less, the same post I put up every January 1st each year. If you are a Delta flyer and don’t live outside the USA you need to either spend your way flying Delta to $3/6/9/15,000 of NET spending to reach each Medallion® level of Silver, Gold, Platinum or Diamond. Oh that, and fly a ton of miles since your elite points are based on distance and fare class. But a far simpler way to not have to worry about how much you have spent each year flying Delta is getting a Delta AMEX card(s). <-LINK

Then just send across any combination of the above to reach $25,000 and you are MQD exempt. But before we dive down this spending extravaganza some common scene base rules. We never EVER pay one cent of interest ever to any bank card PERIOD! That is losing big time and winning is earning points for free or as close to net-free as we can.

Thus some of these ideas require you to already have a solid financial situation and have the ability to “float” some heavy cash outlays for a few months and all it is costing you is the opportunity cost to invest those funds elsewhere. Please be really clear on this and notice how much interest I have paid on my Delta Reserve card over the past two years.

Next, a simple goal is mixing up your spend. If you “hammer” anything that is not good. In addition to the below for the next many weeks I will be almost exclusively using my Delta AMEX cards for everything I pay for even though under many of the circumstances I will be passing up 2x, 3x or more opportunities for earnings as I want to get huge spend done and that means the little things get included. Going “all-in” on any of these could result in negative consequences. We want positive results not unintended frustrations.

We all should know that our MQD exempt total that is reflected at our “My Delta” on Delta.com is a combination of any cards you hold and spend on, personal or business combined. It also includes any spend AUs or authorized users on your accounts spend as well. Every few days on Delta.com these numbers are sent over by AMEX and reflected on your account. Once you have met $25,000 how much more you spend does not matter (as far as MQD exempt status that is) and you cannot rollover any spending into the next year – we all start at ZERO each and every year.

But the real question is what counts and what does not because for many years, some things that the T&C state does not count in reality they do. This means, once again, it is time to test a bunch and give you some ideas of how to reach your goal of 25k. I will be testing each of these and as they update I will change them from “testing” to “confirmed” so check back to see how these tests work for me (btw I have little fear that any will not work perfectly).

- Bills (prepay) – CONFIRMED

- Delta travel (prepay via gift cards) – CONFIRMED

- Home owners – CONFIRMED

- Insurance health and life – CONFIRMED

- Property Taxes – CONFIRMED

- Taxes – CONFIRMED

- KIVA – CONFIRMED

- Sams Club – CONFIRMED

- Pharmacies – CONFIRMED

- Kroger, USPS & others – CONFIRMED

- Simon and other malls – CONFIRMED

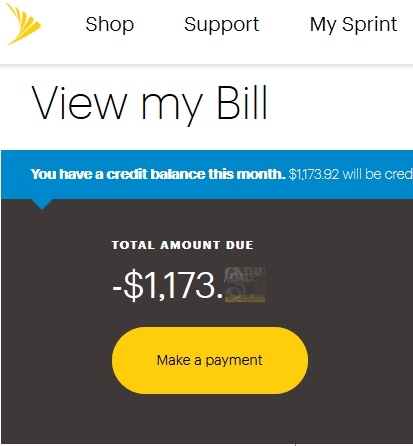

These are the biggest ones that can help you. Let’s look at them one at a time but first start with some simple suggestions. Since being MQD exempt now helps you in scoring more upgrades, the faster you reach this the better. If your finances allow it you may perhaps want to prepay a number of bills for a number of months (or the year for that matter). Your cell, cable, trash pickup and on and on and on. Take the time to look at all the bills you pay on a monthly basis and consider paying so that you have a credit balance for a few months or even for a full year up front (again if your financial situation will allow this). Doing this achieves the MQD exempt spend and helps you so much with bills you have to pay anyway at some point during the year.

Another simple one is basically prepay some of your 2017 Delta travel. You can buy small or large Delta e-Gift cards and then use up to 3 per ticket (plus a credit card) to book your travels. If you plan to spend a bunch anyway this could help you knock out some spend as well up front.

Next up on the list, and a bit outside the box, if you are paying a mortgage very likely you have your homeowners insurance escrowed into the payment. When I was paying for my home I asked to have this broken out and paid it on my own. I used Ameriprise as they were competitive and allowed me to pay the full year on my AMEX card with no fee. Simple and a nice big chunk of my spend done. Think about any kind of expensive spend that can help you rack up what you need each year.

Then we should check with our life, and health insurance and so on. These are of often sizable bills and see if they will take your AMEX card. If they only take DEBIT cards this can still work as you will see in a bit how to work this one.

For me I even paid my property taxes with cards. Depending on where you live some of these ideas may include a small fee of a few dollars to make the payment. It is up to you if it is worth it to pay this way to meet the spend. These extra fee items are a personal choice – is the fee worth the convenience of helping to knock out some massive spend each year. To me, the answer is yes but it may not personally be for you. I am just showing you the option exists (at a cost).

Then we have, what is for some, a way to knock out MASSIVE spend all at once, that is, pay your federal estimated taxes. Yes this spend choice does come with a 1.89% fee but depending on what you value a SkyMile personally at this could be close to a wash. For me I value a SkyMile, when I spend it on a business class award to Europe, at 1.5-2 cents each so you can see the really simple math at making this choice. I can tell you that today I will be making a rather big payment on my estimated taxes with my Delta AMEX Reserve card and I am just fine with the cost included.

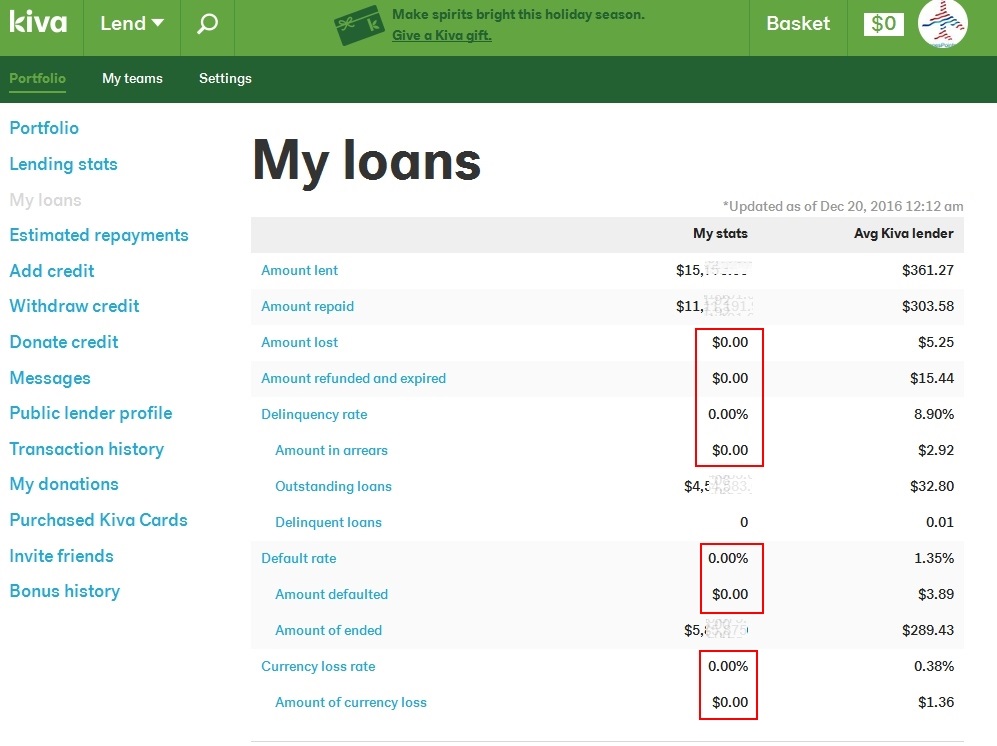

I. Love. KIVA. It is amazing. I get to feel good about helping others and earn points – FREE! Now I am conservative and cautious as a fox, but as you can tell from my results from 2016 it has worked out rather well for me. Yes, I have my money tied up for 6-10 months per loan but the reality, when you have done this for a while and choose well, is that it often gets paid back much faster that expected and you start getting money back very soon. Sure I always try to use my VISA branded FlexPerks card to get 6% back on my money in a about 6 months average but in this case, to help knock out my MQD spend, I am good earning just the SkyMiles to push up my totals.

Did you know Sams Club, and many other places, sell some kind of either Visa or Mastercard Debit gift card. You can figure out the rest on you own. Again, we are talking about mixing up all kinds of spend and this is one more outlet.

Next up we have stores like CVS, Walgreens and so many other locations that offer some kind of gift card for sale. Again, be careful – the point is a mix of spend everywhere you shop.

Speaking about a mix of spend, there currently is almost no end to the locations close to your home that you can visit to buy stuff. Sure with all of these the next step, i.e. using the gift cards in one way or another can be a challenge but there are many places on the web to share advice on how to do just that and at minimal cost to you. If this is a choice for you take the time to learn.

Then we have the gift that keeps on giving – that is, Simon Mall group. They now have a “five back” card. It is a game changer. Take the time to learn about this stunning product. Again, just one more tool to help you with your MIX of spend to get to your MQD exempt goal for 2017!

Lastly we have everything else and it is up to you if it is worth the effort. For example, could you ask your employer to allow you to pay for certain expenses and be reimbursed? Then we can go even deeper and maybe you can ask your family to pay some of their bills (that have no fee) and then they pay you back via a check or cash. This could go on and on if it is worth the effort for you to reach your spend goal.

You see my point in all of this maybe (or least I hope you do). Last year it took me 13 days to be Delta MQD AMEX exempt spend complete. This year I hope to do it in 7 days or less. I am NOT in any way suggesting you do the same. All I am doing is again trying to prove a simple point – you can do it inside one year without too much issue if you want to! That is my point of this 1JAN post year after year after year. – René

Editorial Note: This content is not provided by American Express. Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by American Express. Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

Advertiser Disclosure: Eye of the Flyer, a division of Chatterbox Entertainment, Inc., is part of an affiliate sales network and and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed, or approved by any of these entities. Some links on this page are affiliate or referral links. We may receive a commission or referral bonus for purchases or successful applications made during shopping sessions or signups initiated from clicking those links.

5 Back all the way – I have done so many now it is crazy and GC buying and selling on TPM. I will be completed by Friday for my spend.

Here’s my potential strategy:

Get the Delta Biz Platinum and shift my waiver spend to it. Then when I hit $25K, I get the waiver and the additional 10K MQM boost. $25K is a lot easier to hit than $30K, and I’ll also meet the $5K minimum spend on the Biz Plat without it being “wasted” by not counting toward the waiver spend (it would be nice if waiver spend was the sum of all spending across all DL cards).

Now getting to $25K. I know for sure that I’ll have a few thousand in tuition payments for the summer term, and I’ll start having rent payments come May. I don’t mind paying transaction fees, since they are partially offset by the miles earned, and I consider it worthwhile if the end result is status. I also might be buying a new car, and I’m certain that I can put part of the payment on credit.

Next, I suppose that I will look at dabbling in some Kiva loans. I’m willing to float $10K, so that’s a nice block of spend right there. I’ll need to do more research, but I haven’t seen any horror stories so far.

Finally, I’m going to ask my parents if I can start covering certain payments, such as cell phone, cable, and insurance bills with my card. In exchange, I promise to fly them somewhere on miles at some point.

I’m just not willing to do MOs. I still have a live Bluebird that I might spend into the ground, but I value my relationship with USAA too much. I might do a few small ones if it looks like I’ll fall short, but it’s not going to be the primary method for sure.

I have to do the MQM math carefully. IMO, the lowest level worth putting in the effort to requalify for is PM. Most of the GM benefits I can get by buying paid FC, but PM’s free award redeposit is insanely valuable, as is upgrades that can actually clear at the window, and RUCs. I rolled over 20K MQM this year, and I’ll get 20K more through spend. That leaves 35K to get through flying. My “non-leisure” total last year was 20K, so that leaves just 15K to get with runs, or just a discount TATL biz ticket to visit the grandparents in England.

Sorry for the essay, but I wanted to share my plan to make sure there weren’t any glaring holes in it, and to see if there’s anything in it I can do more efficiently.

@William – Nice. Do listen to my podcast about KIVA. It will help you. Also keep in mind KIVA loans start paying back almost right away so it does not take 6-8 months on a 6-8 month loan to get your money back. It comes month after month and often they pay off loans much more quickly.

What is TPM?

@Bill – I think Kingrat is talking about The Plastic Merchant. I do not recommend this btw.

Happy New Year!! I look forward to this post every year!!

Adding to the point about paying some bills for friends and family: a few family members LOVE my wife & my Amazon Prime membership. We made each family member who uses our Prime account an additional cardholder on our Delta Amexes and told them to order whatever they want — they just need to put it on the credit card bearing their name. This way, when the bill comes, we know right away who owes what. They get the Amazon Prime benefits for free, knock out some of our spend without us having to do anything — and we get the miles (that usually end up paying for some of their trips anyway :-)) and earn the spend threshold and MQM.

@Chris C – BRILLIANT! I love that. My only issue is most of my friends / family are just as into points as I am… grrrrrr 😉

@rene why are you not in favor of TPM?

@Jarred – There are many safer ways.

Rene,

You mentioned “If they only take DEBIT cards this can still work as you will see in a bit how to work this one.” I may have missed it but I didn’t see where you discussed this. Looking forward to this weekend.

@Craig – If you happen to buy a bunch of VDGCs you then have a debit card you can spend on other things (plus they are Visa or MC if something does not take AMEX). 😉

Maybe I’m missing something, but aren’t the MQMs the hard part, not the dollars? That’s certainly my challenge.

The amounts of spending yearly is 3/6/9/12 and not the stated 3/6/12/15 unless this year is different than past year.

@Laurence – it is 3/6/9/15 so we were both off on one number. Fixing!

I had some end of the year charitable giving to do and as it got closer I decided to try using my Delta Platinum to do this on, and to hope that it would count toward my 2017 spend. I did for transactions to four different organizations, late in the day on 12/31… And everyone of them posted on 12/31. I was surprised. If I had thought it though I would have done this a bit earlier and tried to finish out the year with 50k on the card for the second bonus.

Good post

Did it in 5 days. How can I send a screens hot to you? Thanks Rene.

Hi Rene, I just started reading your blog recently and I’ve learned a lot. Thanks for all the great content. I did have a question about the purpose of finishing the $25k spending for the MQD exemption. Since you’re already DM status for the upcoming year, what’s the hurry to finish the spend so quickly? Is it just to be done with it, or is there some other benefit?

@Danny – To show it can be done. Plus, having the 25k spend now helps with upgrade tie-breaker. So I want it in place ASAP each year.

Does paying someone by credit card through paypal work?

@Adobo – Have not tested but would not see why not. The fee is rather high. There are cheaper options.

Another option for us is the kennel for pets. Ours favorite place runs promotions from time to time, and we KNOW we are gonna need them for all those free vacations thru the year.

Re: Paypal, yes, you can set AMEX as your preferred payment method. Switched to that today after reading this blog, and it seems to work just fine.

Rene, I had forgotten about this post & just read it again. I did some of these things to easily reach $50k this year. As a retired banker, Kiva still makes me very nervous. Also the Simon 5% cash back is ending 11/1/17.

I’m still not sure how to convert a visa debit card back to cash. Sure I can use it to purchase where AMEX is not taken, but I don’t buy $21k worth of stuff in a normal month. I don’t mind the fee for the card if I could turn it back into cash some way. If this is possible, I hope that you will include information on that along with any new ideas that you may have when you update this post. Thanks!

@Bill – You need to come to Chicago Seminars!

Rene, I’ve got a conflict on 11/21, so I cannot attend. I will watch for the dates of the next one as I think I can learn enough about points/miles strategies to justify the small cost. And it will probably be fun as well. The $250k spend may still be out for me & I am beginning to question if DM is really worth it anymore. I have been DM every year since it started…was a “Charter” member. One of the best perks of DM has been GU. They are now very difficult to use on popular routes. Most only clear at the gate if they clear at all. When they do not clear, somehow there is still room in business for non-revs. I wonder what the hierarchy for upgrades is with Delta? Anyway I’ll look for the next seminar dates.