Advertiser Disclosure: Eye of the Flyer, a division of Chatterbox Entertainment, Inc., is part of an affiliate sales network and and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed, or approved by any of these entities. Some links on this page are affiliate or referral links. We may receive a commission or referral bonus for purchases or successful applications made during shopping sessions or signups initiated from clicking those links. The content on this page is accurate as of the posting date; however, some of the offers mentioned may have expired.

Talk about a brick wall.

I mean a solid as a rock brick wall.

What wall? you ask.

The new-ish rule from Chase that if you have applied for more than 5 credit cards (including authorized users from any bank) in the past 2 years (yes that is 24 months as you see above) you have ZERO chance of being approved for many Chase cards. Soon, it seems, all of them including co-branded cards and business cards as well.

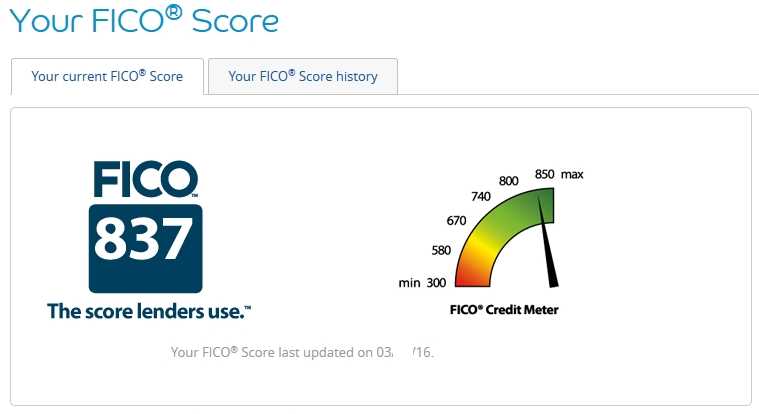

Notice the credit score above. What stands out to you. Maybe the fact that it is just a few points away from a “perfect” score? Yeah, I am impressed with my wife’s score.

My wife decided, for the points yes but also for testing purposes, to go for a new Chase Sapphire card because it had been a while (years) since she had one. The result when calling in to see if there was a way to get approved (since there was no instant approval) was NO. No moving of credit lines around and no chance to speak to a supervisor or anyone else. She was told this was a “policy decline” and no one could change that at Chase bank to approve the card. Period!

Now keep in mind the same day she was approved for four other credit cards.

Now with AMEX we have to be careful, if we want a new card bonus, that we have never had THAT specific card bonus before but even if you have had that, under the new rules with AMEX, you can still at least get the card again – just not the bonus.

See why the Chase rule is so nasty and long term just a stupid rule for the bank? They are flat out blocking you for LIFE to ever get most cards EVER again (unless you are willing to wait 2+ years between card applications).

Even if you just want it to use as a card with no bonus. Something to keep in mind if you currently HOLD certain Chase cards.

These are interesting times in the world of travel cards. As many have reported at some point this month the 5/24 rule from Chase will engulf co-branded as well as business cards. If there are any of these types of cards you are thinking of going for, if you delay much longer, you may be out in the cold (for good)! – René

Featured image: ©iStock.com/zwawol

Advertiser Disclosure: Eye of the Flyer, a division of Chatterbox Entertainment, Inc., is part of an affiliate sales network and and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed, or approved by any of these entities. Some links on this page are affiliate or referral links. We may receive a commission or referral bonus for purchases or successful applications made during shopping sessions or signups initiated from clicking those links.

I’m trying to follow your logic here of why its stupid for Chase to block someone that is freely admitting that they are only applying for cards for the bonus. I’m not passing judgment, I do the same thing and love it, I’m just trying to understand why you think the AMEX policy is better when they both effectively prevent you from getting the bonus. Have you ever (or plan to in the near future) applied for a card that didn’t have a bonus? Is that why you prefer the AMEX rule?

@Mike – As mentioned, if the card is not in the users hands there is NO chance for swipe fees for the bank. Don’t get me wrong, the AMEX policy is horrid as well but at least if you want some card you can get it today!

Obviously I don’t love the rule either, but when you look at how many cards your wife applied for that day, it’s hard to say that Chase is being completely stupid.

@James K – I hold and use my Chase Sapphire card. How do you know my wife would not do the same? Clearly now she will not and they will lose out on all those swipe fees. #JustSaying

Rene since when have they started counting AU’s????

@Greg – It has been reported they are counting them as well. At least from some readers. 🙁

@Rene, that’s a real bummer about AU’s. I guess Chase wants to eliminate customers in general. It’s not just churning they are stopping with this policy. Let’s say you get added to SOs two credit cards and pick up 1.5 cards a year…bam you are at 5/24. I wish they’d just limit bonuses or something.

Unfortunately I think Chase knows the swipe fees will never make up for the cost of the bonus for the vast majority of churners. There may be exceptions, but not enough.

I don’t like the Chase policy, but overall I’m sure it will add to the bottom line, and therefore can’t call it a stupid business decision.

@Carl P – You are not looking at big picture. I know of one HVC that had a home loan with Chase and went in and paid off and closed Chase accounts over non-approval. There will be bigger implications.

Not surprising. I had a phone call with Chase yesterday for a new Marriott card and it was like pulling teeth but they finally “did me a favor” and approved it. I think it’s a good business plan for Chase but it might catch up with them. There are plenty of non-churners that apply for 5 or more cards over 2 years. It’s like throwing the baby out with the bath water at some point (pardon the pun).

If I was chase I would allow you to open the card without the bonus. There is no reason not to I would think.

@DaninMCI – Agree. I think they should (gasp) either change to AMEX rule or better yet if they want the current rule up the total to say 8 or 10 cards in two years. Even those who do not keep going for cards over and over can get 5 cards in two years way too easy with just life and offers in the mail they may go for.

Makes me think they also consider churners unprofitable from the swipe fees standpoint. Their cards aren’t explicitly rigged with an assinine redemption process (like A+, Thankyou, etc.) to try to force breakage and using your points below their full potential. Their stats like show that churners maximize bonus categories, point use, etc…

Who knows, maybe enough dollar volume leaves their cards that they’ll rethink it.

The bonus on this new card is small potatoes. Getting, and by corollary using, this card for 1.5 UR’s on everyday spend is very good. Add the ability to combine points from the CSP(or Bold) and this is a decent value proposition.

IMO, Chase turning down applicants for this new card who are proven heavy CSP users is myopic.

I just got approved for the Chase Sapphire and had to speak to the customer service folks after they initially turned me down because of the 5/24 rule.

When I explained that two of these cards were only as Authorized User on my wife’s accounts they then approved me.

My wife also got approved for the Chase Marriott card even though she has had more than five new accounts opened in the past two years.

@Matthew – Txs for yet another confirmation on AU counting but that they can possibly overlook them.

Yes, for now, co-brand and business are not under 5/24 but are on the way soon!

I’m still unhappy about the amex rule though I’m the only one to blame for mycircumstances. I got my one and only Amex card back before there was such a thing as bonus miles for applying. Thus, Ive never applied for another one because I already had one and wouldn’t get the bonus on a new one. I am considering applying for a business card, get the bonus and then close the old one. I don’t see the sense in paying two yearly fees so I limit the amount of cards I carry. Don’t bother telling me about all the other wonderful bonuses because im delta captive and Hilton captive because of my travel cities. I’m beginning to think that carrying a cash back bonus card with no fees will be sufficient for my needs.

Took a 10 minute phone call to the recon line(due to an identity issue) but was approved by moving a bit of credit around.

I’ve had wayyyyyyyyyy over 5 cards in the last 24.

@Sarah – There are plenty of other Amex cards you could get the bonus on. If, for example, you have a Delta card, then you won’t be able to get the bonus on Delta again. But Platinum, Premier Gold, Everyday, Blue Cash, etc., should be fine to get a bonus.

@Greg N – Not totally correct. All 3 Delta cards are unique (as well as biz cards). So you can get EACH ONE once and get the bonus.

I think that part of the problem is that with Chase, you need either Ink Bold or CSP in order to convert whatever you generate on Freedom or Freedom Unlimited into Ultimate Rewards points, so that makes it multiple cards immediately in order to maximize their program, irrespective of the bonus offers. And considering Bold has different bonus spend categories, and Freedom and Freedom Unlimited have different types of bonus spend, you need to get 4 total cards in order to maximize a person’s spending patterns even for someone not looking at churning. So Chase is losing out on someone possibly devoting all of their spend on their cards if that person was churning elsewhere.

I was just approved for the Chase Freedom after getting at least ten credit cards since January. I got the AMEX SPG and Chase Sapphire Preferred® Card first. I have paid both cards either before they were due, or immediately upon receiving the statement. I have continued to use the Chase SF as my go-to card, and I pay the bill immediately. I was able to move available credit from my Chase IHG card to the Chase Freedom when I called after getting a “pending approval” response when I applied for the Chase Freedom.

I’ve decided that my best long-term plan is to use the Chase SF and Freedom for my spending, at least until they change their terms.

This is a frustrating way to see the world, but I’m in with both feet.