Advertiser Disclosure: Eye of the Flyer, a division of Chatterbox Entertainment, Inc., is part of an affiliate sales network and and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed, or approved by any of these entities. Some links on this page are affiliate or referral links. We may receive a commission or referral bonus for purchases or successful applications made during shopping sessions or signups initiated from clicking those links. The content on this page is accurate as of the posting date; however, some of the offers mentioned may have expired.

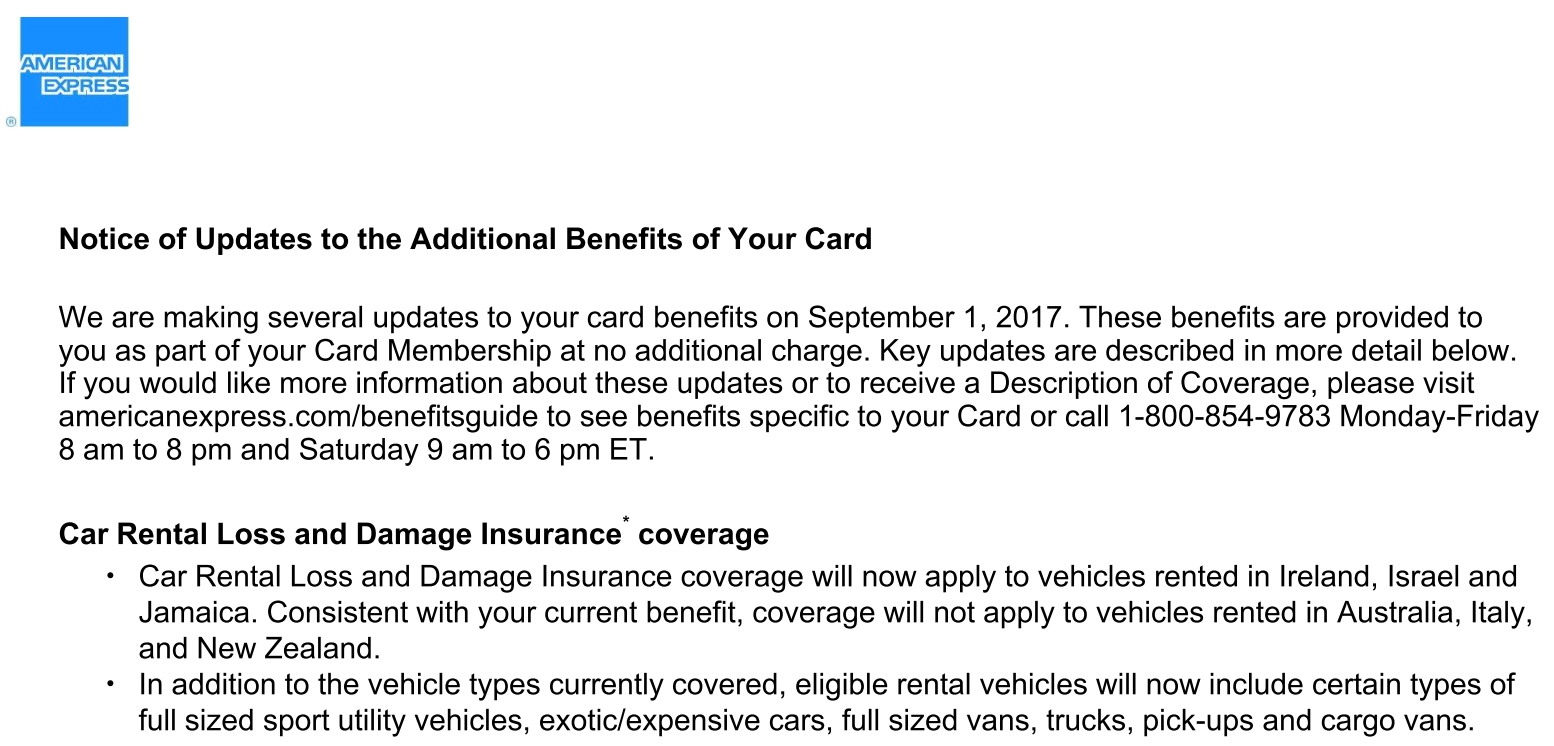

Across all my cards (and my wife’s cards including CO-branded cards) AMEX has informed us that as of September 1st the car rental insurance provided when you pay for the rental with your AMEX card has improved.

What has changed? First, some of the vehicles that were excluded are now included. This matters because you may get an “upgrade” to some amazing exotic car but the problem is the retail price for the car is so much that your protection you thought you had is not in place. We need to read the T&C and not just assume folks!

Next up we have a number of countries what were excluded are now included. They are Ireland, Israel and Jamaica. This really is a BIG and important change because most of these can really soak you for forced added insurance. Do notice some countries are still excluded and they are Australia, Italy and New Zealand.

While these changes are nice they really do not go far enough for me. Over 4 years ago I wrote a series of posts about what card provides the best insurance option (Amex or Visa) and the advice still mostly is valid. Visa, and ideally a Visa that included primary coverage, is still the best choice for a normal every day rental. However, the AMEX changes do shake things up and now MUST be considered. Why?

The current Visa auto rental coverage (PDF file) does still exclude exotic cars. Amex “may” cover you (but be sure to call before you rent to confirm). Visa also excludes rentals in Ireland, Israel and Jamaica. So we can see, under certain circumstances, Amex now provides better coverage!

Bottom line these are positive changes from Amex and I hope Visa will follow them with similar improvements in coverage. – René

Advertiser Disclosure: Eye of the Flyer, a division of Chatterbox Entertainment, Inc., is part of an affiliate sales network and and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed, or approved by any of these entities. Some links on this page are affiliate or referral links. We may receive a commission or referral bonus for purchases or successful applications made during shopping sessions or signups initiated from clicking those links.

Thanks for explaining that. I got a headache attempting to read all of those pages of fine print!

Hey Rene now you have 31 perfect reasons to get the Amex Delta Platinum card 🙂

@DDiamond – I just had not had time to get to rental insurance but happy I waited as this change does make it winner under some circumstances yes!

I recently had a claim for a window chip ($125) on a car I had rented using the Delta Platinum Amex card. They refused to pay because they claimed my own car insurance would pay it, notwithstanding the fact that I would never file a claim this low and risk my premiums going up. After much back and forth between American Express and my insurance company, I concluded (and it was confirmed by my insurance company) that their so-called coverage is complete b.s. since there is no instance in which they would ever pay a claim. I’ve been meaning to send them a letter because I’m completely outraged by this — all these years I actually thought they were providing coverage, but haven’t gotten around to it yet.

@JP – That is why Visa cards with primary is so important from cards like the Chase Sapphire Reserve® for example.

I do have a Chase Sapphire Reserve® and that’s what I’ll use in the future. It just makes me so angry because I always thought I was covered by Amex, especially since they advise you to decline the CDW. But when something happens, they just tell you to file any claim with your own insurance company.

P.S. The reason they wouldn’t even pay out up to my deductible is because I have rental coverage for when my car is in the shop, and that coverage also pays the deductible in the event you have an accident with a rental car. So Amex pays nothing. Ever.

Last summer I backed into a gas station guardrail after I filled up prior to returning my rental car. Stupid me. While waiting for my flight I called Am Ex and was transferred to the insurance company. I filed the claim over the phone. IMO the $15 fee that covers rentals up to four weeks is a bargain. They paid the $1K claim without any hassles.

@Wayne – Agree. I also have the upgraded Amex rental (the $25 one) when/if I rent with Amex. That program is rock solid vs the fee default one.

I’ve been relying on my CSR exactly because it offers primary coverage. BUT note that you may still want some of the other coverages for personal injury as my understanding is the card’s coverage only includes damage to the vehicle itself.

@AT – Agree. As mentioned in the other posts you want Visa perks AND you own insurance. If you do not own a car pay for the Amex upgraded protection (again see linked posts)!

I found out afterewards, while renting an SUV – required for winter snow driving in Switzerland to get safely up the mountains with your ski-gear – that I was NOT covered at all with my Amex because of the type of car – an Audi – that I was assigned at the check-out in ZRH.

Go figure !

In addition to this hiccup, I was told last month – while renting at DEN airport through my Citi ThankYou points that “no rental through points/miles is ever covered by a credit card’s insurance” !

Was the agent correct ?

I cannot find any other info on this unfortunately

@GV – See linked posts. With UR points from Chase you are (at least you were 4 years ago, I would confirm today as well). With TY points not sure.